M&A Advisor Tip

What happens to employees after I sell?

Business owners often come to us concerned about employee jobs and retention issues after a sale. They worry that selling their business will lead to job losses if certain positions become redundant.

However, buyers today are often just as focused on retention issues. Your experienced talent can be a key value driver, and buyers want to make sure these people stick around.

Your management team is the highest priority retention target, and deal structures will often involve some sort of retention bonuses or shareholder equity options for top leadership. Many buyers, particularly private equity, will consider management retention incentives a routine cost of doing the deal.

While the remaining employee group is less likely to receive financial incentives, buyers ARE looking at culture, communication, and change management. Today, HR is more likely to be involved early in the process in an effort to help the organizations blend culture rather than impose new corporate will.

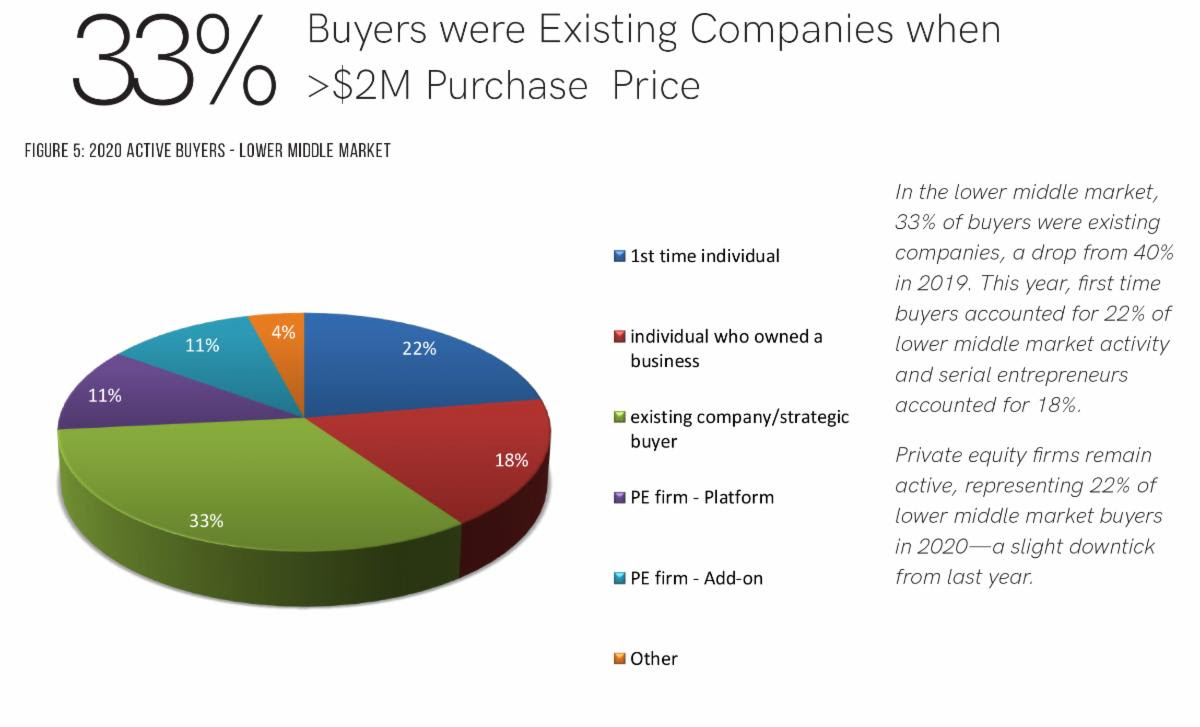

Market Pulse Survey - Quarter 4, 2020

Presented by IBBA & M&A Source

M&A Feature Article

SBA to cover six months payments on new loans

As part of the Economic Aid Act that passed in December, the Small Business Administration will make borrowers’ payments for six months on new SBA 7(a) and 504 real estate and micro-loan programs.

These incentives were available last summer under a stimulus program that expired in September 2020. Now the program has been revived and enhanced.

The SBA will make the first six months of payments (principal and interest) on new loans approved between Feb. 1 and Sept. 30, 2021. To be clear, these payments will be covered, not deferred or pushed back to the end of the loan period. Payments are capped at $9,000 per borrower per month.

The Section 7(a) loan can be used to buy a business or used for working capital, equipment, or inventory. Qualified borrowers can access up to $5 million.

The SBA’s 504 microloan program can be used for assets that grow your business, including land, facilities, facility improvements, and long-term equipment investments. These loans have similar limits and requirements as the Section 7(a) loans.

Would-be borrowers will have to get approval through an SBA lender. But the good news here is that the new law has increased the federal guarantee for the loans from 75% under last year’s program to 90% this year for most loans. That lowers the risk for lenders and makes it easier for them to extend financing.

Borrowers with existing loans will receive an additional three months of payments and interest, starting February 2021. (These borrowers previously received automatic payment assistance from the SBA.) Plus, borrowers in the hardest-hit industries, such as restaurants, salons, entertainment, arts, and recreation, can receive an additional five months of payments.

The law appears to be written with the intent that the SBA will cover loan origination fees which are 2.5 to 3.5% of the loan amount. That’s something we hoped was coming last summer, but ultimately didn’t come to fruition.

On a loan of $5 million, SBA fees could be about $138,125 or more. That’s free money for buyers who move now and get their loan issued soon. While the program is set to end on September 30, 2021, it could be closed earlier if all funds have been exhausted.

While the law has been approved, the SBA and Treasury Department were still fleshing-out the final rules at the time of writing. The SBA maintains a list of authorized lenders on its website. We recommend reviewing a lender’s SBA loan closure rate to ensure you’re working with an experienced, responsive lender.

If you are acquiring a business, your M&A advisor or investment banker should be able to recommend active SBA lenders with a track record of success.