Advisor M&A Tip

What is Dry Powder?

You may have heard about the unprecedented level of "dry powder" in the market. In the M&A world, we refer to dry powder as the cash reserves businesses keep on hand to fund acquisitions or future business investment. In the last few years, private equity firms have amassed record amounts of investor dollars, aka dry powder. These firms are under considerable pressure to deploy those assets and generate returns for their investors.

The more dry powder there is in the market, the more pressure there is to use that money (i.e., acquire businesses). This pressure increases competition and drives up multiples. And, it's created a wider buyer pool for businesses in the lower middle market as private equity firms shift their focus down market in order to find new opportunities.

Market Pulse Survey -2nd Quarter 2019

Presented by IBBA, M&A Source and in Partnership with Pepperdine University

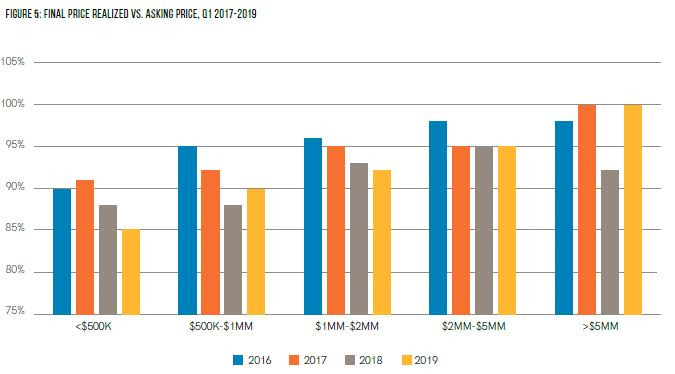

Where Are Business Values Trending?

"Private equity is extremely active in the lower middle market, and that's pushing values upward," said Craig Everett, PhD, director of the Pepperdine Private Capital Markets Project at the Pepperdine Graziadio Business School. "Industry reports suggest private equity has nearly $2.5 trillion in unspent cash right now. Many of them are shifting resources down to the Lower Middle Market in order to maximize their chances of winning a deal and putting that cash to work."

M&A Feature Article

Earnouts Don't Deserve A Bad Reputation

When selling a business, an earnout is basically a commitment by the buyer to pay the seller a certain amount of money tied to future performance after a sale. While earnouts are a great way to boost the value of your company, they can be a dicey proposition for a seller.

Even if you stay on with the business, you don't have complete control over how new ownership runs the company. If the business does well, you get paid. If business drops, you don't.

Most times in the M&A world, earnouts are used as a last resort to bridge a value gap between the seller's expectations and what the buyer believes the company is worth. They can be particularly useful in certain situations:

One good year: Let's say your business had an amazing year last year, significantly higher than the past. You might be selling the business with the expectation that your recent performance is the new normal. Meanwhile the buyer is thinking something along the lines of, "But you've only done this once."

In this scenario, the buyer will typically offer a price based on some weighted average of historical performance. By tacking on an earnout, you get some of the upside if the business continues to perform the way you believe it will.

Customer concentration: Businesses that attribute 20 percent or more of sales to just one customer represent a particular risk for the buyer. The higher the concentration, the higher the risk. Earnouts allow the buyer to mitigate some of that risk by hinging some value on their ability to keep that client.

Recent investments: We're representing a company that made a $6.5 million investment in their business just six months before going to market. They have solid projections and believe this investment will create a sizable income stream in the future.

But they've just started to market this new service, and there's little to no proven revenue. In this case, we can expect a buyer will pay the value of the asset at close. However, an earnout arrangement will reward the seller if business projections come to fruition.

Overall, earnouts get a bad rap. Perhaps you've heard of someone who never got paid. Or maybe you've been advised not to expect a dollar of an earnout agreement.

I think those fears are somewhat unfounded, particularly when agreements are negotiated by an experienced M&A attorney. I can assure you, buyers would love to pay that earnout. The alternative is that their new business is not hitting financial projections or they lost a key customer, and that's not where buyers want to be.

That said, there's certainly a way of structuring deals to reduce seller risk. As a seller, you probably don't want an earnout tied to cash flow, because the new owners can manipulate that bottom-line number. But buyers don't want to pay earnouts based on revenue because your team could rack up sales at razor thin margins.

Most of the time we recommend that earnouts are tied to a percentage of gross profits, with a clear formula as to what's included in cost of goods. That way, the buyer is still getting a firm margin while you're getting assurances they can't manipulate the numbers.

As a seller, your willingness to accept an earnout sends a sign of confidence to a buyer. This signal of faith can reduce a buyer's fears and help get a deal across the finish line.

We recently reached out to a few past sellers to see how their earnout arrangements were going. In each case, sellers had received all or a majority of their earnout benchmarks to date. That's good news all around, as it means those acquisitions are doing well under new ownership.

So if your M&A advisor brings up the word earnout, don't run the other way, and don't close your mind. It could be an opportunity to gain additional value in your company, especially if there are unique circumstances or if you truly believe the upside is great for the new buyer.