M&A Advisor Tip

Agree on ‘What if?’

Beware of setting up partnerships in which two or more people have equal ownership and power in decision making. If you do, you need some kind of buy/sell agreement in which one or both partners can get out at a fair price.

Rather than a traditional shotgun clause, which could leave an undercapitalized partner with less than fair market value, consider one that relies on a third-party valuation. We recommend getting an affordable estimate of value every few years to establish a realistic benchmark.

No matter how strong your friendship is at the outset, it’s good to plan a “what if” clause if things go sour. If you can’t decide on that, don’t enter a partnership at all.

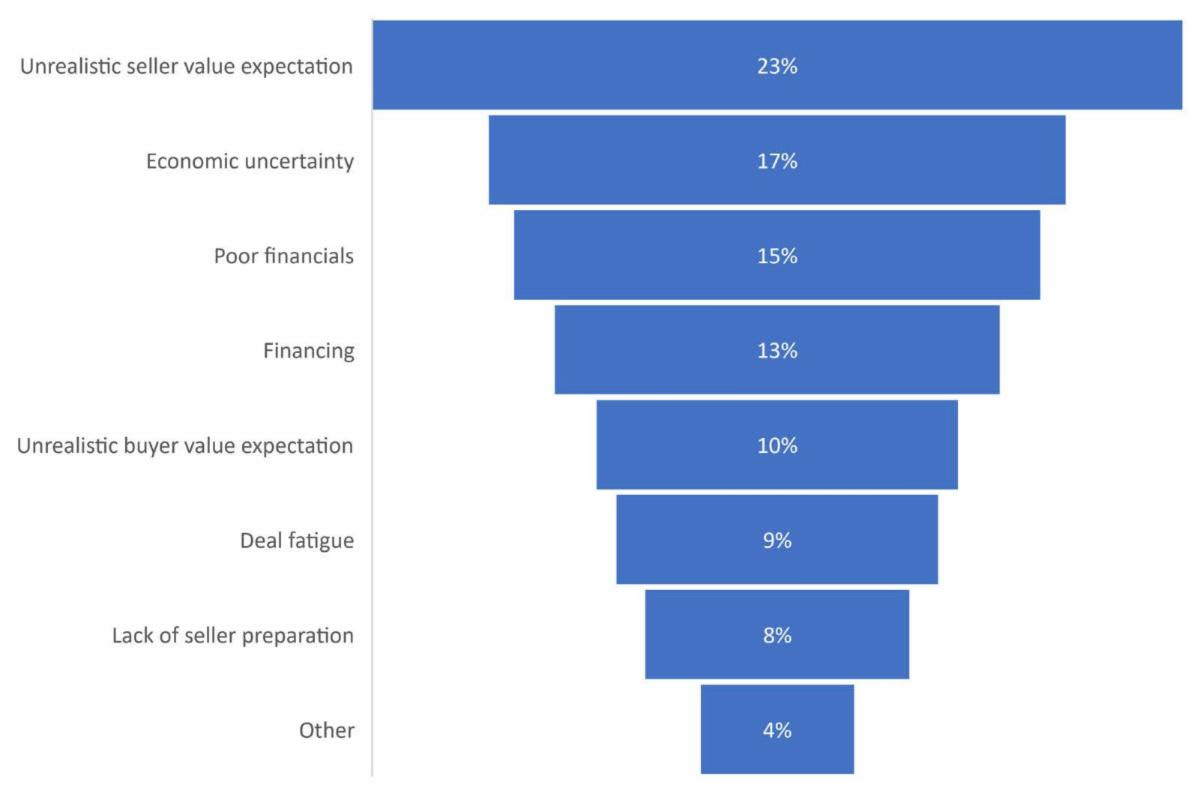

Market Pulse Survey - Q4 2022

M&A Feature Article

Supply chain issues complicating M&A

Supply chain issues are a big concern for businesses right now. Forced shutdowns, crisis forecasting, labor issues, and logistics all played (or are still playing) a part in the current shortages. Business has not snapped back to normal.

Managing the supply demand imbalance will be a tricky problem for at least the next six months, if not the next year or more ahead. And it will complicate M&A transactions for business owners looking to sell.

Supply issues are affecting M&A in a couple of ways:

Supplier due diligence. We’re seeing buyers do supply chain due diligence like we never have before. In the past, buyers were relatively relaxed about supply issues, but now they’re looking for multiple suppliers, length of supplier relationships, strength of supplier operations and more.

We brought one business to market this year that had backups and prototypes for nearly every single product component. Frankly, we’d never seen a company put so much time and energy into supplier redundancies.

And yet, they had one essential circuit board without an alternate supplier. And that circuit board is the issue every potential buyer honed in on. Buyer concern was so significant, we eventually decided to take the business off the market until a reliable secondary supplier could be identified.

Working capital. The other problem with supply issues comes at the tail end of an M&A deal in working capital negotiations. We predict this will be one of the most hotly negotiated deal points in 2022.

Working capital is like gas in a car – you need to sell a car that runs. When selling a business, a certain amount of net working capital is left in the business to meet standard operating needs.

Generally, the seller keeps the cash in the checking account and pays off the long-term debt at the time of the sale. What stays in the business is the inventory, plus accounts receivables (A/R), minus accounts payables (A/P)—that’s considered the working capital. In a typical economy, we calculate this on a 12-month average to arrive at our “working capital peg.”

But right now, many businesses are building up larger than normal inventory levels to compensate for shortages and delays. Manufacturers that used to buy inventory on a just-in-time basis are now buying just-in-case.

Not only are inventories larger than normal, but in many cases the price-per-unit has skyrocketed as well. Businesses are paying whatever they have to in order to get critical parts in stock.

So let’s assume that in normal times the business kept 100 widgets in stock, but now they’re inventorying 200 widgets. And in month 12 before selling the business, the price of those widgets doubles.

As a seller, you still want to calculate working capital on the 12-month average. But the buyer says that average isn’t nearly what they need to run the business for the year ahead. They might want the seller to take a haircut.

This is one of the areas that can really upset sellers – being asked to leave money on the table near the end of negotiations. The good news is that with all the competition on the market, we could see buyers willing to concede on working capital negotiations in order to keep the deal.

It’s also a good idea to address working capital at the front end of negotiations. Historically, it was common for M&A firms to accept a letter of intent (an offer letter) with vague terms around a “mutually agreeable working capital number” to be arrived at later. Today, we recommend sellers and their advisors stipulate exactly how working capital will be calculated before accepting offers.